Our Expert says

Bank Rates Are Now Lower But Is Switching Right for Everyone?

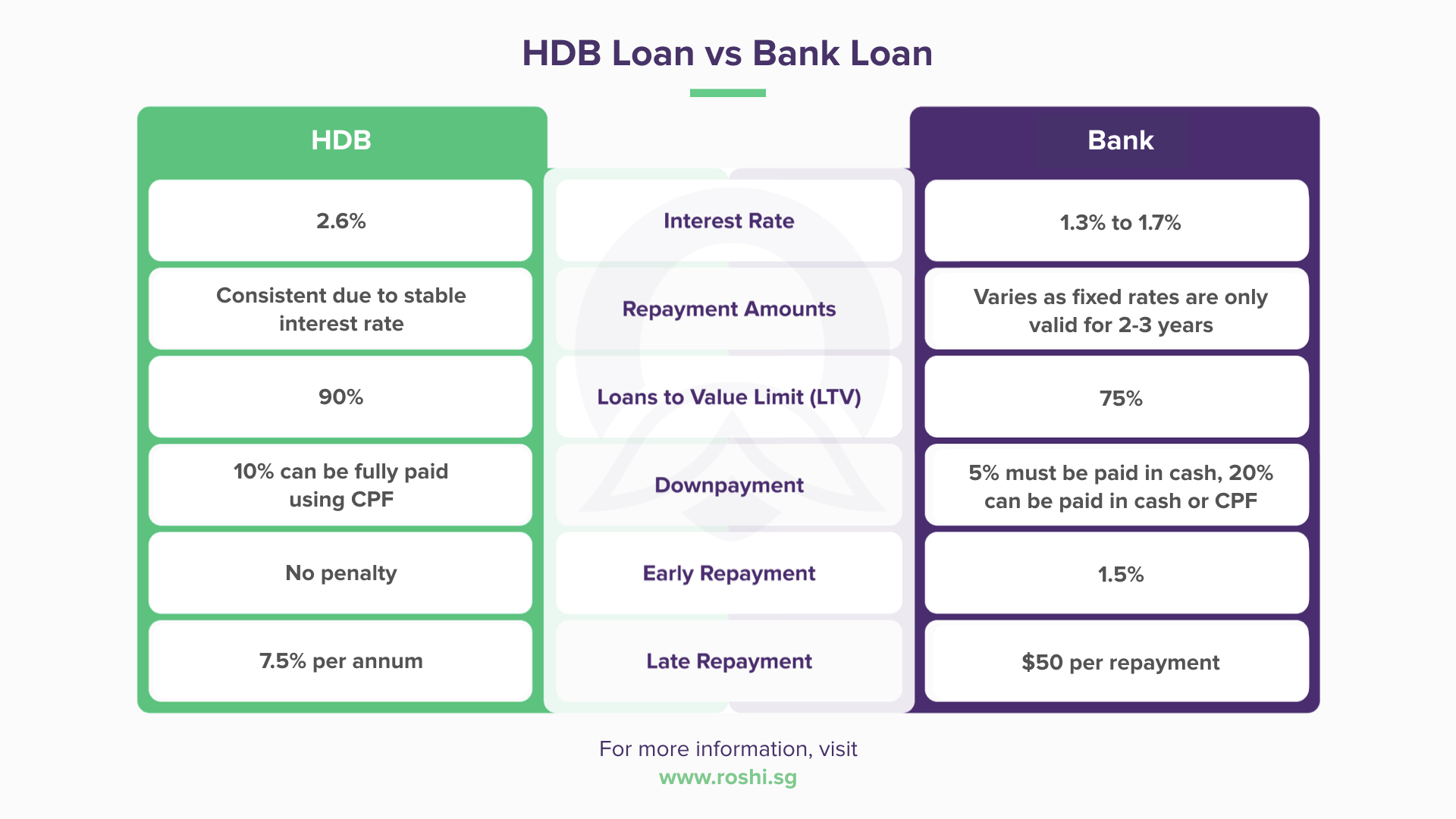

With bank rates at 1.50% to 1.75% versus HDB's 2.6% savings are significant, roughly $200 per month on a $400,000 loan. However, HDB loans offer stability, no lock-in and the flexibility to refinance later without penalty.

For first time buyers unsure about rate movements, starting with an HDB loan keeps options open. For those confident in their finances and comfortable with a 2-year lock-in, a bank loan delivers substantial savings. Our calculator helps compare both scenarios side by side.: ![]()

![]()

HDB Loan Eligibility Criteria

Who Qualifies for an HDB Loan?

At least one applicant must be a Singapore Citizen

Must form a family nucleus (married, engaged, single 35+, etc.)

Gross monthly household income below $14,000 (for new flats)

No existing property ownership

Must not have taken 2 or more HDB loans previously

MSR below 30% of gross monthly income