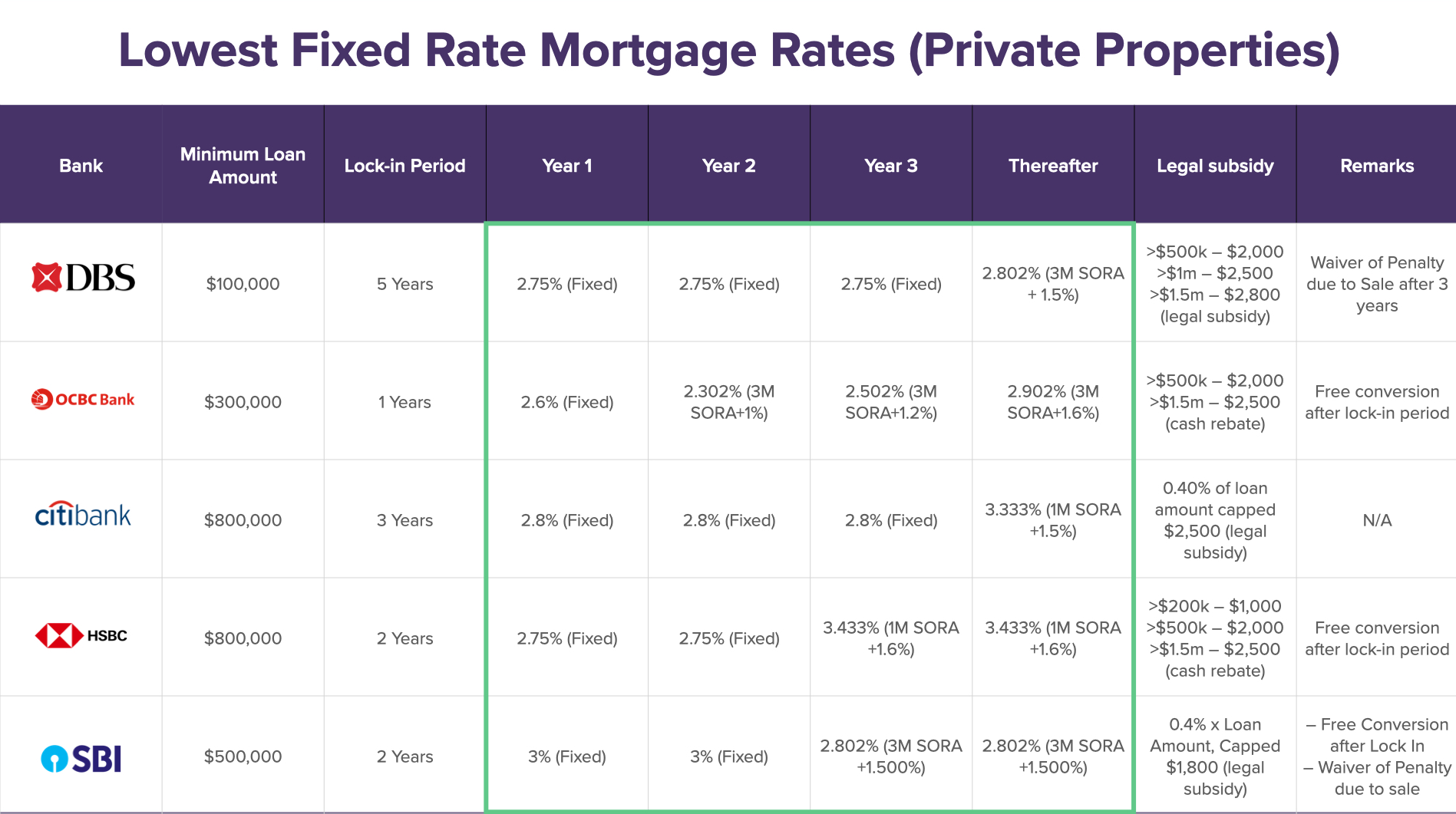

Bank refinancing rates start from 1.50% p.a. (fixed) and SORA+0.25% (floating). HDB concessionary loan rate is 2.6%.

Refinancing a home loan is one of the most effective ways to reduce monthly mortgage payments and save

tens of thousands of dollars over the life of a loan. This

page covers everything there is to know about refinancing in Singapore: how it differs from repricing,

when refinancing makes financial sense, the costs & common

fees, eligibility requirements including TDSR rules and a breakdown of the entire process. It also

explains the key considerations for HDB flat owners switching

from an HDB concessionary loan to a bank loan and how private property owners can access home equity

through cash out refinancing.

Whether the goal is to secure a lower interest rate, switch from fixed to floating or restructure your

loan tenure this page provides the information needed to make a more informed decision.

Refinancing is the process of replacing an existing home loan with a new one from a different bank. The new bank pays off the old loan and issues a new mortgage — typically with a lower interest rate, different loan structure, or better features. Refinancing is commonly done when lock-in periods end and homeowners want to take advantage of lower market rates.

Bank refinancing rates start from 1.50% p.a. (fixed) and SORA+0.25% (floating). HDB concessionary loan rate is 2.6%.

A 1% rate reduction on a $500,000 loan saves approximately $220 per month or $2,640 per year. Over 10 years, that's $26,400+.

Most banks offer $2,000 to $2,800 in legal fee subsidies for refinancing. Additional cashback may also be available.

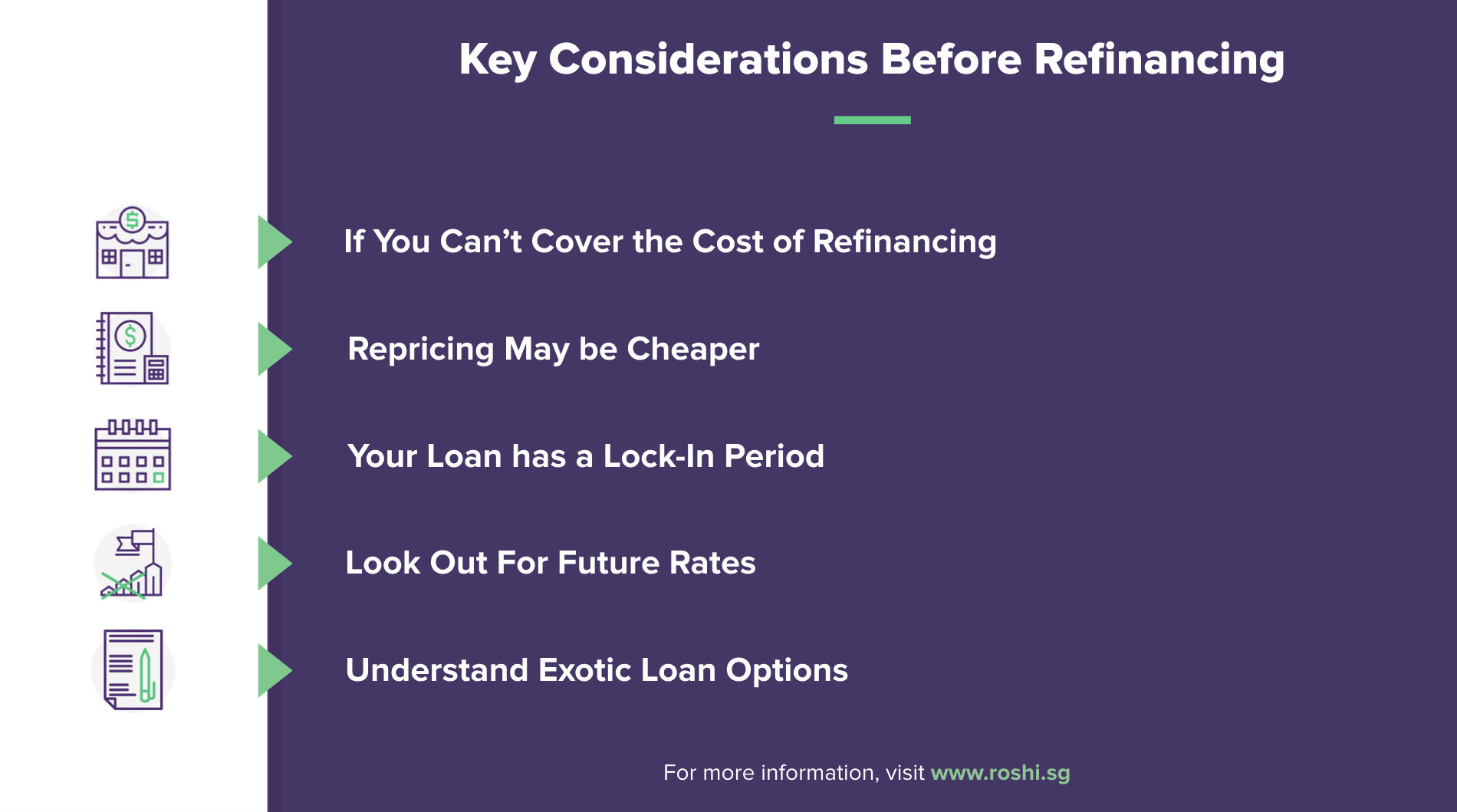

Start comparing 4 to 6 months before lock-in ends. The refinancing process typically takes 3 to 4 months to complete.

| Refinancing | Repricing | |

|---|---|---|

| Definition | Switch loan to a different bank | Switch package within same bank |

| Interest Rates | Access to "acquisition rates" typically lower | "Retention rates" may be 0.1% to 0.3% higher |

| Timeline | 3 to 4 months | 1 month |

| Legal Work Required | Yes | No |

| Valuation Required | Yes | No |

| Costs | $2,000 to $3,000 (often subsidised) | $500 to $1,000 (admin fee) |

| Lock-In Period | New 2 to 3 year lock-in | May be shorter or none |

| Loan Options | Access to all banks' packages | Limited to current bank's packages |

| Documentation | Full application with income docs | Minimal — internal bank process |

| Best For | Larger loans above $300k, maximising savings | Smaller loans below $300k, convenience |

| Flexibility | Full market access | Limited to one bank's offerings |

| Option | New Rate | Annual Savings | Costs | Net Savings (3 years) |

|---|---|---|---|---|

| Refinancing | 2.7% (Bank B) | $4,900 | $2,000 (subsidised) | $12,700 |

| Repricing | 3.0% (Same bank) | $2,800 | $800 | $7,600 |

Banks typically offer lower "acquisition rates" to attract new customers and higher "retention rates" to keep existing ones. This pricing gap often 0.1% to 0.3% is sometimes called the "loyalty tax."

On a $1 million loan that difference can cost an extra $2,000 per year. For larger loans above $300,000 refinancing to a new bank almost always makes more financial sense than repricing with the current bank. For smaller loans below $200,000, the legal and valuation fees may outweigh the savings making repricing the more practical choice. The key is to calculate the total savings against total costs before deciding.

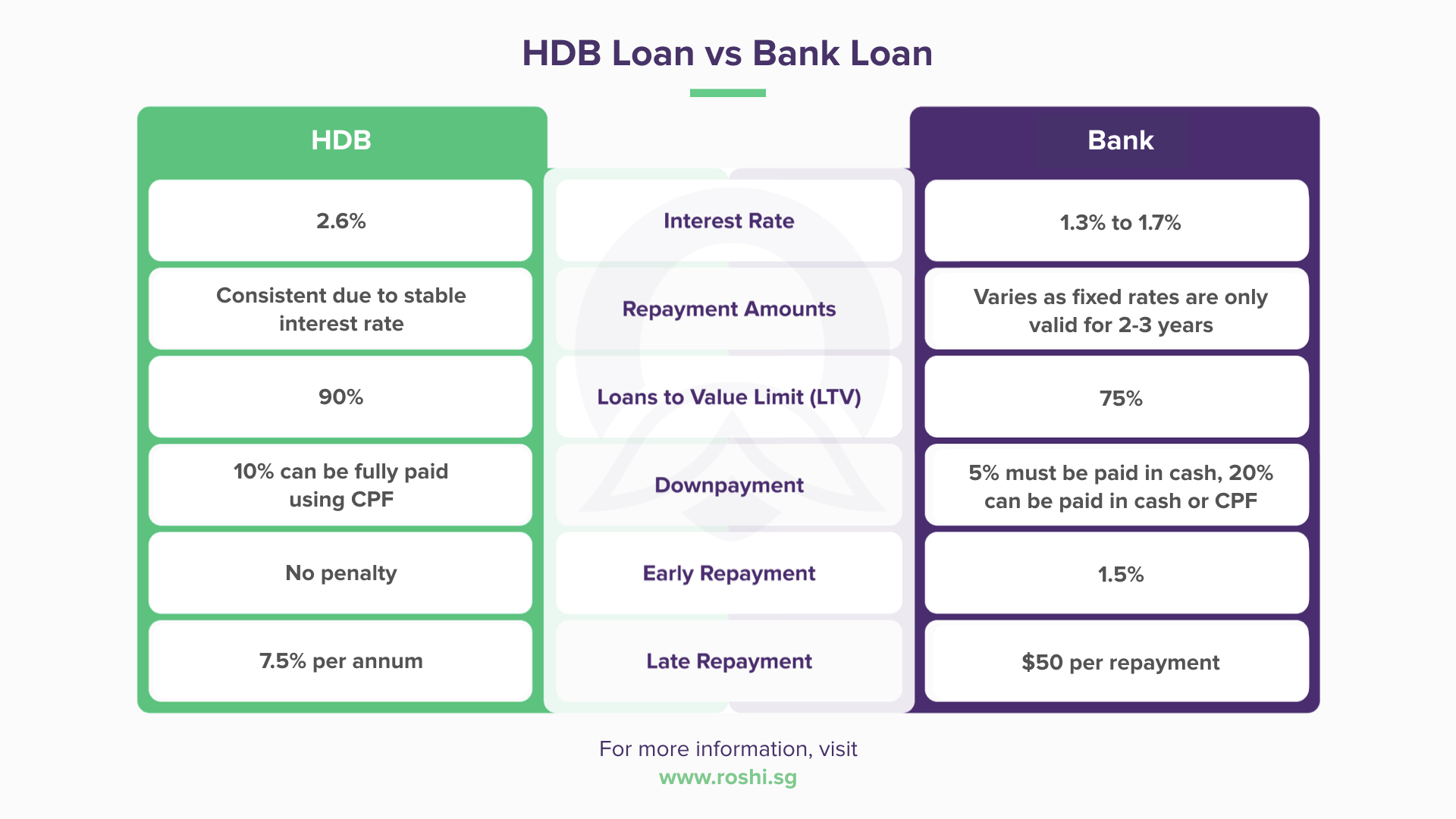

| HDB Concessionary Loan | Bank Loan (After Switch) | |

|---|---|---|

| Interest Rate | 2.6% p.a. (fixed) | From 1.50% p.a. (fixed) or SORA+0.25% (floating) |

| Rate Stability | Extremely stable (unchanged 20+ years) | Fixed for 2 to 5 year then floating OR floating from start |

| LTV After Switch | N/A | Up to 75% |

| Lock-In Period | None | 2 to 3 years |

| Early Repayment Penalty | None | 1.5% during lock-in |

| Partial Prepayment | Allowed anytime | May be limited during lock-in |

| Rate Fluctuation Risk | None | Yes |

| Can Switch Back? | N/A | Irreversible |

| TDSR Applies? | No (exempt) | Owner-occupied: exempt for refinancing / Investment: applies |

| Cost Item | Refinancing | Repricing |

|---|---|---|

| Legal fees | $1,800 to $2,500 | Not required |

| Valuation fee | $300 to $600 | Not required |

| Administrative fee | $0 to $500 | $500 to $1,000 |

| Total Costs | $2,100 to $3,600 | $500 to $1,000 |

| Legal subsidy from new bank | $2,000 to $2,800 | Not applicable |

| Net Cost After Subsidy | $0 to $1,000 | $500 to $1,000 |

| Property Type | Owner-Occupied | Investment |

|---|---|---|

| Refinancing (same or lower loan amount) | Exempt | Exempt |

| Refinancing with cash-out | Applies | Applies |

| Repricing (same bank) | Exempt | Exempt |

With rates at multi-year lows and SORA around 1.1% to 1.2%, 2026 is an excellent time to refinance. Here's practical advice for different situations:

For HDB owners on bank loans: The promotional rate from 2-3 years ago has likely expired. Compare rates now, a 0.5% to 1% reduction is common and translates to significant savings.

For HDB owners on HDB loans (2.6%) : Bank rates are now well below 2.6%. The decision to switch is significant because it's irreversible. Calculate savings, consider rate fluctuation risks and decide based on personal risk tolerance.

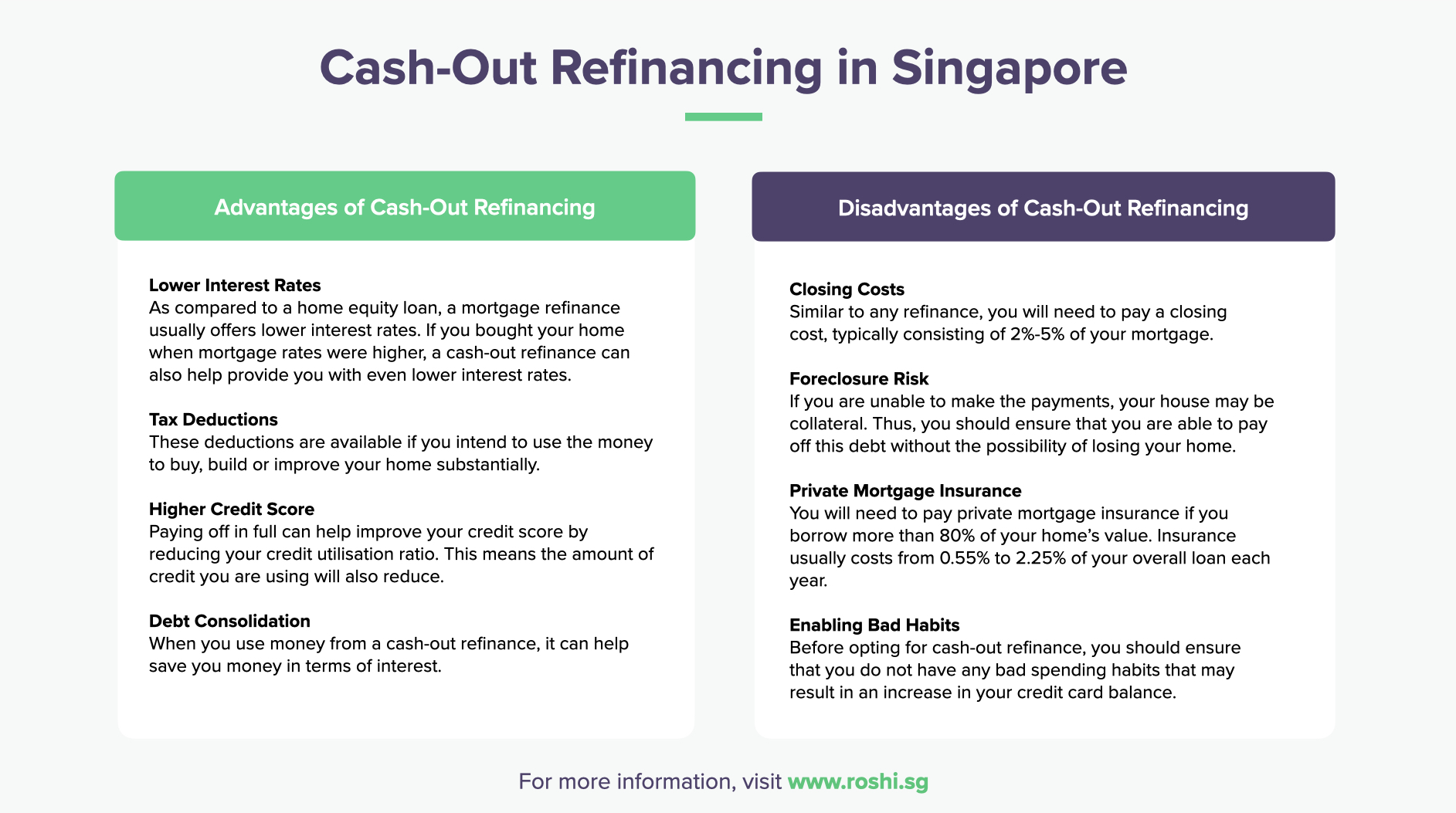

For private property owners: Beyond rate shopping, consider whether cash out refinancing makes sense for investment or debt consolidation goals. Ensure any additional borrowing is within comfortable repayment capacity.

Rate tip: Don't just look at Year 1 rates. Check the spread after lock-in (Year 3+). A package with a lower Year 3 spread gives more buffer before the next refinance cycle.

Timing tip: Don't wait until the last minute. Start comparing 4 to 6 months before lock-in ends. Banks need 2 to 3 months to process and there's often a "lag cost" of paying the higher rate while waiting for the switch.

Rate tip: Don't just look at Year 1 rates. Check the spread after lock-in (Year 3+). A package with a lower Year 3

spread gives more buffer

before the next refinance cycle. ![]()

![]()

| Outstanding Loan | Monthly Savings | Annual Savings | 3-Year Savings |

|---|---|---|---|

| $200,000 | $130 | $1,560 | $4,680 |

| $400,000 | $260 | $3,120 | $9,360 |

| $600,000 | $390 | $4,680 | $14,040 |

| $800,000 | $520 | $6,240 | $18,720 |

| $1,000,000 | $650 | $7,800 | $23,400 |

I used ROSHI platform to find the best loan offers. Just need to fill up some details and wait for loan offers and can choose which one you like. It is totally free and can receive vouchers and cashback based on the loan amount approved. Thank you ROSHI

I can’t thank Roshi enough for helping me find the best financial institution for my DCP! The guidance and support were absolutely amazing—everything was explained clearly and tailored to my needs. Thanks to Roshi’s help, I’m now on track and completely debt-free in just 12 months! 💪🏼 I couldn’t be happier with the outcome and highly recommend Roshi to anyone looking for smart, reliable financial advice.

With the help of the ROSHI Support link to partner, I had a great experience with EZY Loan. The online application was simple, document verification was fast, and the funds were credited on the same day. The staff were professional and explained everything clearly, with no hidden fees. Overall, an excellent and hassle-free service!

Roshi service will update all your listings to match your nearest requested amount accurately, saving you time and effort by eliminating the need to visit each location individually. Recommended !

Your home is going to be one of the biggest purchases you will ever make in your life.

A cash-out refinance is an option that replaces an old mortgage with a new home loan.

Refinancing consists of replacing a current loan with a new one that pays off the debt of the first loan.

Refinancing is when you fully repay your existing home loan or move your loan to a rival lender

Your decision to refinance your home loan can be due to certain common reasons such as taking cash out, getting a lower payment, or to shorten your mortgage term.

Most Singaporeans buy a HDB flat to live in it, that’s a fact.

Refinancing is not the only way to optimise a mortgage. For homeowners looking to access cash from their property's value without selling, home equity loans offer a way to unlock funds for personal or business investment needs. Home buyers purchasing a new property can compare home loan rates from 15+ banks .

For quick estimates on potential savings when switching to a lower rate, our refinance calculator compares current repayments against new rates and factors in costs to determine if refinancing makes financial sense.

For bank specific refinancing packages and features, reviews are available for local banks including DBS, OCBC and Maybank as well as foreign banks such as Standard Chartered, HSBC, Citibank and Bank of China.