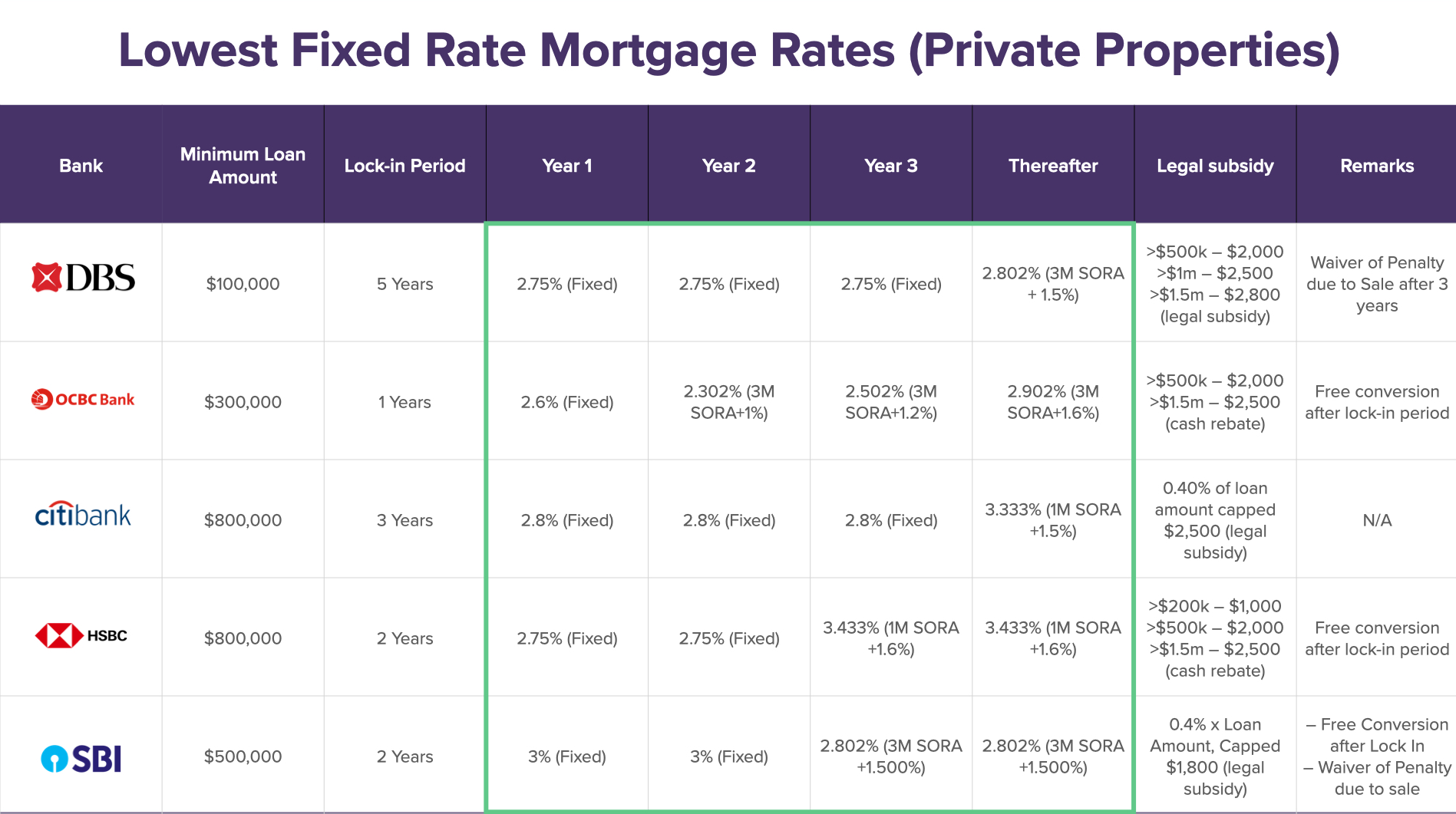

Our Expert says

Start Comparing 4 to 6 Months Before Lock-In Ends

The most expensive mistake in refinancing is waiting too long. Once the lock-in period ends the loan typically reverts to a higher rate (e.g., SORA+1.0% instead of the promotional 1.75%). Every month spent at the revert rate while waiting for a new loan to process is money lost.

My advice, start comparing rates 4 to 6 months before lock-in ends, apply 3 to 4 months out and time the new loan to begin exactly when lock-in expires. This calculator helps determine if the savings justify the effort but timing is just as important as the rate itself. ![]()

Refinancing Costs Breakdown

Understanding All Refinancing Costs

Quick Affordability Reference:

| Cost Item | Amount | Notes |

|---|---|---|

| Legal fees | $1,800 to $2,500 | Often subsidised by new bank |

| Valuation fee | $300 to $600 | Sometimes subsidised |

| Admin/processing fee | $0 to $500 | Varies by bank |

| Total gross cost | $2,100 to $3,600 | - |

| Legal subsidy (new bank) | $2,000 to $2,800 | Most banks offer this |

| Cashback (if any) | 0 to $500 | Varies by bank/promotion |

| Net cost after subsidy | $0 to $1,000 | Often minimal |

Clawback clauses:

If current bank provided subsidies within 2-3 years, may need to repay them

Lock-in penalty:

If refinancing before lock-in ends, 1.5% of outstanding loan applies

Notice period:

Most banks require 2-3 months notice factor this into timing